Snapchat filed for an IPO with the SEC on Februrary 2, 2017 expecting to be priced at $20-$25 Billion from the share offering. I have no clue whether it is fairly priced given that I know very little about the company. Hence, I have decided to value the company more out of curiousity rather than being a prospective investor (I can't invest even if I want to).

The Business Model

Before I dive into number crunching, I need to get a sense of what business they are in, the market size and market dynamics, and identifying their competitors. Going through their S-1 filing with the SEC, The company defines itself as a "camera company" and primarily has three product categories:

1. Snapchat- The camera cum chat application is the main growth driver for the business. The below graph shows the different functionalities of Snapchat:

2. Publisher Tools

This is where Snapchat generates it's revenue. These tools enable companies to create advertisements and these can be targeted to users either using Snap stories above or creating Sponsored lenses and filters wherein companies create a Sponsored lens of their product. Also, They are able to generate revenue through Snap Ads, which are video advertisements played in Snap stories.

3. Spectacles

The first hardware product by the company, Spectacles are essentially sun glasses that enable you to record a snap and wirelessly enable you to add it to the Snapchat App. Launched in 2016, This is another potential revenue stream for the company.

Market Size and Competition

To come up with an estimate for the market, I did a google search and got my hands on emarketer's estimates (although they are a bit old). As of 2016, the digital mobile advertising market was $101.37 Billion, 40.2% of the total digital advertisement spending. The market is projected to grow at a CAGR of 24% till 2019 whereas the total digital advertising market is projected to grow at an annualized rate of 12%. I have backed out the digital advertising market size using the numbers in the article.

Using this article, I have updated emarketer's estimates for 2016 and 2020. The 2016 year end spending is expected to be $194.60 billion globally and the market is expected to reach a size of $335 billion in 2020. This translates into an annualized growth rate of 14.54%. The high growth in digital advertising is being driven by mobile advertising, which is expected to be 73.7% of total digital advertising market in 2020.

Using this article, I have updated emarketer's estimates for 2016 and 2020. The 2016 year end spending is expected to be $194.60 billion globally and the market is expected to reach a size of $335 billion in 2020. This translates into an annualized growth rate of 14.54%. The high growth in digital advertising is being driven by mobile advertising, which is expected to be 73.7% of total digital advertising market in 2020.

I also had a look at Snapchat's direct competitors in the online advertising space (Mentioned on Page 18 of S-1 filing as well):

Clearly, Google and Facebook account for more almost 55% of the market share based on revenues. Facebook has been paricularly impressive, beating analyst expectations quarter after quarter and is now generating an operating margin higher than Google. Compared to other players, Snapchat is a currently a small player and is making no money. An interesting story here is that of Twitter, The company performance has been continuously going downward and it has failed to capitalize and generate more advertising revenues from its existing user base. With rumours floating around that Twitter is for sale, It will be a huge task for the company to gain market share against competitors like Google and Facebook.

After taking a look at the company's business model as well as the market and competition, My thoughts about the same are summarized below:

1. Competitive Advantages: In my opinion, The two key advantages that Snapchat has are 1) The Snap vanishing in 15 seconds and 2) Potential networking benefits. The App is particularly popular among the age group of 18-24 because the content you send vanishes after 10-15 seconds and in that age group you do tend to send a lot of stuff which you don't want anyone to have a record of. Combining this with potential networing benefits i.e. the popularity among friends acts as an impetus for other friends to join the App. This has enabled the company to have Average Daily Active Users(DAU's) of 158 Million as of Q4 2016.

2. Monetizing Users: Still a long shot?: Although Snapchat has been able to substantially increase it's revenues by almost 700% from 2015 to 2016, I believe there will be challenges in further scaling up the business and increasing revenues. One reason is of course operating in an extremely competitive space and going up against competitors like Google and Facebook. The other concern stems out of their business model. Sponsored filters and lenses are a great tool to spread the awareness of a new product and make it viral but cannot efficiently communicate the different features of the product. Moreover, Facebook through Instagram has brought out it's own Story feature in response to Snap story and get a share of the video advertising pie.

3. Corporate Governance Red Flag: While going through the S-1 filing, A particularly scary information stood out: The shares being offered are Class A shares i.e. these shares do not have any voting rights. The voting power is concentrated in the hands of Evan Spiegel and Robert Murphy through Class C shares, accounting for 88.6% of total voting power. This effectively means that there will be no significant authority to question the co-founders for their business decisions and the goal of creating firm value might get undermined by vested self interests. Therefore, I will have to build this lack of corporate governance in my valuation.

4. The mystery of Spectacles: One potential source of revenue generation that I haven't discussed much is Spectacles. The revenue for Snapchat from spectacles remains minimal as evidenced by their disclosure that the Spectacles revenue was not material in 2016. With a $130 price tag, I find it kind of hard to see it developing in a mass market product. Products similar to Spectacles have not had much success (read Google Glass) and it's main competitor is rear camera of your smartphone. I am not sure whether there is a market there which will actually enable Spectacles to become a huge success, atleast there is no tangible evidence of that yet.

Building the Narrative

After taking a look at the company's business model as well as the market and competition, My thoughts about the same are summarized below:

1. Competitive Advantages: In my opinion, The two key advantages that Snapchat has are 1) The Snap vanishing in 15 seconds and 2) Potential networking benefits. The App is particularly popular among the age group of 18-24 because the content you send vanishes after 10-15 seconds and in that age group you do tend to send a lot of stuff which you don't want anyone to have a record of. Combining this with potential networing benefits i.e. the popularity among friends acts as an impetus for other friends to join the App. This has enabled the company to have Average Daily Active Users(DAU's) of 158 Million as of Q4 2016.

2. Monetizing Users: Still a long shot?: Although Snapchat has been able to substantially increase it's revenues by almost 700% from 2015 to 2016, I believe there will be challenges in further scaling up the business and increasing revenues. One reason is of course operating in an extremely competitive space and going up against competitors like Google and Facebook. The other concern stems out of their business model. Sponsored filters and lenses are a great tool to spread the awareness of a new product and make it viral but cannot efficiently communicate the different features of the product. Moreover, Facebook through Instagram has brought out it's own Story feature in response to Snap story and get a share of the video advertising pie.

3. Corporate Governance Red Flag: While going through the S-1 filing, A particularly scary information stood out: The shares being offered are Class A shares i.e. these shares do not have any voting rights. The voting power is concentrated in the hands of Evan Spiegel and Robert Murphy through Class C shares, accounting for 88.6% of total voting power. This effectively means that there will be no significant authority to question the co-founders for their business decisions and the goal of creating firm value might get undermined by vested self interests. Therefore, I will have to build this lack of corporate governance in my valuation.

4. The mystery of Spectacles: One potential source of revenue generation that I haven't discussed much is Spectacles. The revenue for Snapchat from spectacles remains minimal as evidenced by their disclosure that the Spectacles revenue was not material in 2016. With a $130 price tag, I find it kind of hard to see it developing in a mass market product. Products similar to Spectacles have not had much success (read Google Glass) and it's main competitor is rear camera of your smartphone. I am not sure whether there is a market there which will actually enable Spectacles to become a huge success, atleast there is no tangible evidence of that yet.

Building the Narrative

My story for Snapchat is as follows:

Snapchat is a social media company which generates it's revenue primarily from online advertising. It will be able to leverage on it's competitve advantages to increase market share. Given it's business model and competition, Snapchat will not be the largest player in the market.

Connecting the Numbers

1. Revenues

I have assumed that Snapchat will generate revenues of $19.81 Billion in Year 10. To come up with this number, I have made the following assumptions:

1. Using emarketer's estimates, I have assumed a annualized growth of 14.54% for the first five years for the digital online advertising market. Therefore, the market size in Year 5 is $383.7 Billion. I give Snapchat a market share of 1.5% in Year 5, which gives me revenues of $5.7 Billion in Year 5. The market share might seem low as I am giving them a share of total digital advertising market, not just mobile advertising. This translates into an annualized growth rate of 70.12% from Year 1 to Year 5.

1. Using emarketer's estimates, I have assumed a annualized growth of 14.54% for the first five years for the digital online advertising market. Therefore, the market size in Year 5 is $383.7 Billion. I give Snapchat a market share of 1.5% in Year 5, which gives me revenues of $5.7 Billion in Year 5. The market share might seem low as I am giving them a share of total digital advertising market, not just mobile advertising. This translates into an annualized growth rate of 70.12% from Year 1 to Year 5.

2. To come up with revenues in Year 10, I linearly decline the growth rate from Year 5 to growth rate of the economy in Year 10 i.e. 2.41%. I am building in the fact that Snapchat's business model and existing competition will be a challenge in increasing number of users and monetizing them. I also believe that given their networking advantages and popularity among the age group of 18-24, they will be able to eat into market share of Twitter, which is grappling with it's own troubles of stagnant revenue growth. Therefore, revenues for Snapchat 10 years from now are $20.29 Billion i.e. 5 years of high growth followed by linear decline to economy growth rate in year 10. The revenue figure is lower than Facebook and Google's current revenues, which means that I am assuming that Snapchat would be a smaller player than both of them.

2. Margins

Currently, Snapchat has an operating margin of -96.68%, which I have adjusted by treating operating leases as debt and capitalizing R&D expenses. I have assumed an operating margin of 22.50% for Snapchat 10 years from now i.e. the average operating margin for internet software firms globally. Being in a highly competitive business, I believe any margins higher than industry average will be hard to come by for Snapchat. I am also factoring in the fact that Snapchat is currently in a high growth phase of it's life cycle and it will be more focused on increasing it's user base. This should translate into more revenues but put pressure on the margins. Here as well, I am giving them an operating margin lower than Google and Facebook.

3. Reinvestment

To come up with Snapchat's renivestment, I have assumed a Sales to Capital Ratio of 1.10 for Snapchat. The current Sales to capital ratio for Snapchat is 0.40 and the global industry average sales to capital ratio is 0.80. I am implicitly assuming that Snapchat will become more efficient over time and will generate higher sales for every dollar of capital invested. The implied return on invested capital in year 10 is 13.99%.

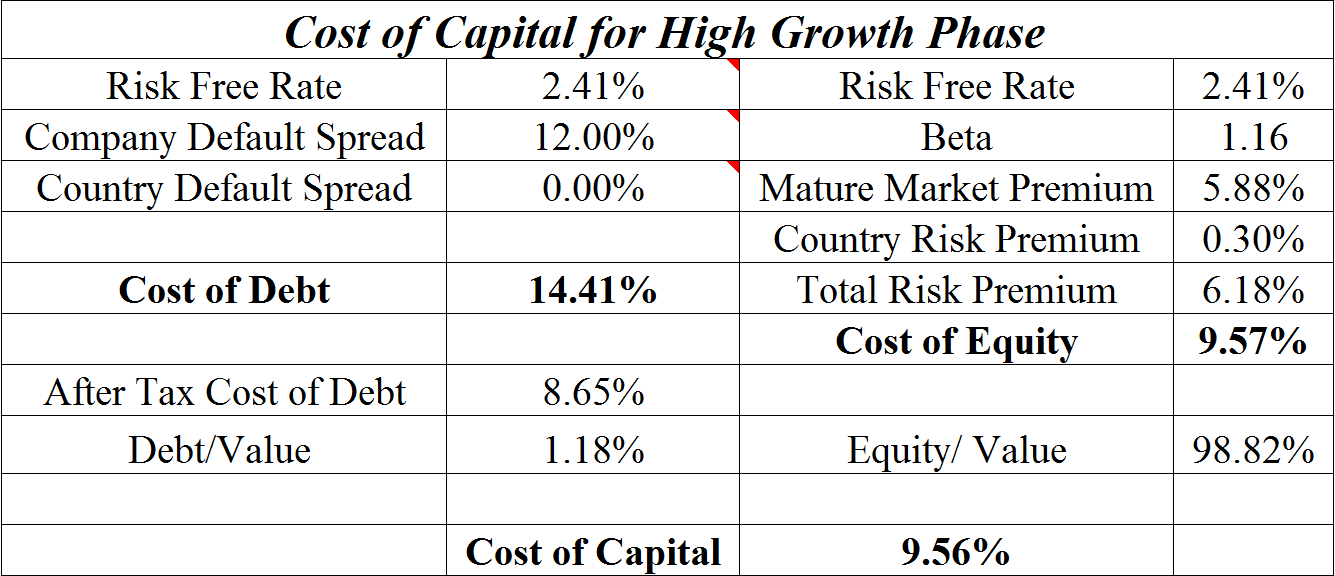

Cost of Capital

Stable Growth Assumptions

1. Growth Rate- I have assumed that growth rate of the company in perpetuity will be equal to the risk free rate i.e. 2.41%.

2. Cost of Capital- I have assumed that debt and equity weights will converge to industry average weights alongwith beta converging to market beta of 1. As the company's borrowing capacity increases when it starts making money, I have also assumed that company default rating will transition from D to Baa3 (the lowest investment grade rating).

3. Return on Invested Capital- This is where I build in my concerns regarding corporate governance issues. Whereas the average internet software company has a spread of 6.50% between return on invested capital and cost of capital, I have assumed only a 4% spread. This will lead to higher reinvestment, lower terminal value and will reduce the value of the firm.

Value of the Firm and Equity2. Margins

Currently, Snapchat has an operating margin of -96.68%, which I have adjusted by treating operating leases as debt and capitalizing R&D expenses. I have assumed an operating margin of 22.50% for Snapchat 10 years from now i.e. the average operating margin for internet software firms globally. Being in a highly competitive business, I believe any margins higher than industry average will be hard to come by for Snapchat. I am also factoring in the fact that Snapchat is currently in a high growth phase of it's life cycle and it will be more focused on increasing it's user base. This should translate into more revenues but put pressure on the margins. Here as well, I am giving them an operating margin lower than Google and Facebook.

3. Reinvestment

To come up with Snapchat's renivestment, I have assumed a Sales to Capital Ratio of 1.10 for Snapchat. The current Sales to capital ratio for Snapchat is 0.40 and the global industry average sales to capital ratio is 0.80. I am implicitly assuming that Snapchat will become more efficient over time and will generate higher sales for every dollar of capital invested. The implied return on invested capital in year 10 is 13.99%.

Cost of Capital

Stable Growth Assumptions

1. Growth Rate- I have assumed that growth rate of the company in perpetuity will be equal to the risk free rate i.e. 2.41%.

2. Cost of Capital- I have assumed that debt and equity weights will converge to industry average weights alongwith beta converging to market beta of 1. As the company's borrowing capacity increases when it starts making money, I have also assumed that company default rating will transition from D to Baa3 (the lowest investment grade rating).

3. Return on Invested Capital- This is where I build in my concerns regarding corporate governance issues. Whereas the average internet software company has a spread of 6.50% between return on invested capital and cost of capital, I have assumed only a 4% spread. This will lead to higher reinvestment, lower terminal value and will reduce the value of the firm.

Discounting the Free cash flows to the firm alongwith the terminal value at the cost of capital gives me a firm value of $9.50 Billion. Subtracting out market value of debt of $298.96 million brings me an equity value of $9.18 Billion. Here, I subtract out the value of 22.45 million options outstanding i.e. $174.01 Million and add on cash and marketable securities of $3.98 Billion (which includes $3 Billion that Snapchat will raise from the IPO) to finally arrive at a value of equity of $13 Billion. Dividing this by number of shares outstanding i.e. 1.3 Billion (includes 200 million new shares that will be issued in the IPO) gives me a value per share of $10.01.

Factoring in the Uncertainity

1. Market Implied Variables

Since the issue will be priced between $14 to $16, I have backed out the implied revenues and operating margin in Year 10 using goal seek for a share price of $15. The implied revenues in Year 10 are $33.9 Billion whereas the implied operating margin in Year 10 is 31.30%. Given my narrative about company's business model and the business environment, these figures seem to be overly optimistic.

2. Monte Carlo Simulation

To capture changes in my assumptions, I did a Monte Carlo simulation wherein I gave a uniform distribution for revenues in Year 10 and a triangular distribution for operating margin in Year 10. After 1,000,000 simulations, The median value per share is $8.31. There is a 80% certainty that the value will be between $6.36 and $10.57.

Bottomline

The Snap IPO story is indeed an intriguing one: The company does have competitive advantages that will work for it. However, the real test of scaling up the business begins now. Personally, I believe the IPO will be priced at the lower end of the price spectrum given that the company has more to prove in terms of it's growth story and corporate governance issues stemming out of its shareholding structure. I will be following the company closely after the IPO to see if there is any informaton that might cause me to revisit my story and valuation.

Link to Valuation Model

Note: Please do not consider any content on this blog as an investment recommendation or advice. At the time of posting of this article, I do not have any financial interest in the company being analyzed. The views reflected in this blog are my personal views and have been arrived at using public information sources.